Is Harvey Too Cheap?

How law firm leaders should think about the impact of VC subsidies

Katon Luaces

Exploring the “True Cost” of AI Tools

Last week at a conference in Santa Cruz, I got into a few discussions regarding the cost-basis of AI vendors. The central question can be captured by “Is Harvey too cheap?”

By “Harvey,” I am less interested in Harvey, the specific AI company currently valued at ~5 billion. I don’t even mean Harvey, the product created by the company Harvey. Instead, I mean Harvey as a stand-in for the third wave of legal technology (more to come on legal technology waves) products that depend on leading commercial foundation model providers (e.g., OpenAI and Anthropic).

And by “overpriced”, I do not mean relative to their value. There is plenty written debating the return on investment from these tools. Instead, I mean relative to their cost-basis. That is, if all venture capital and temporary government subsidies were removed, what would we expect “Harvey” (or the myriad of other tools with similar architectures) to cost?

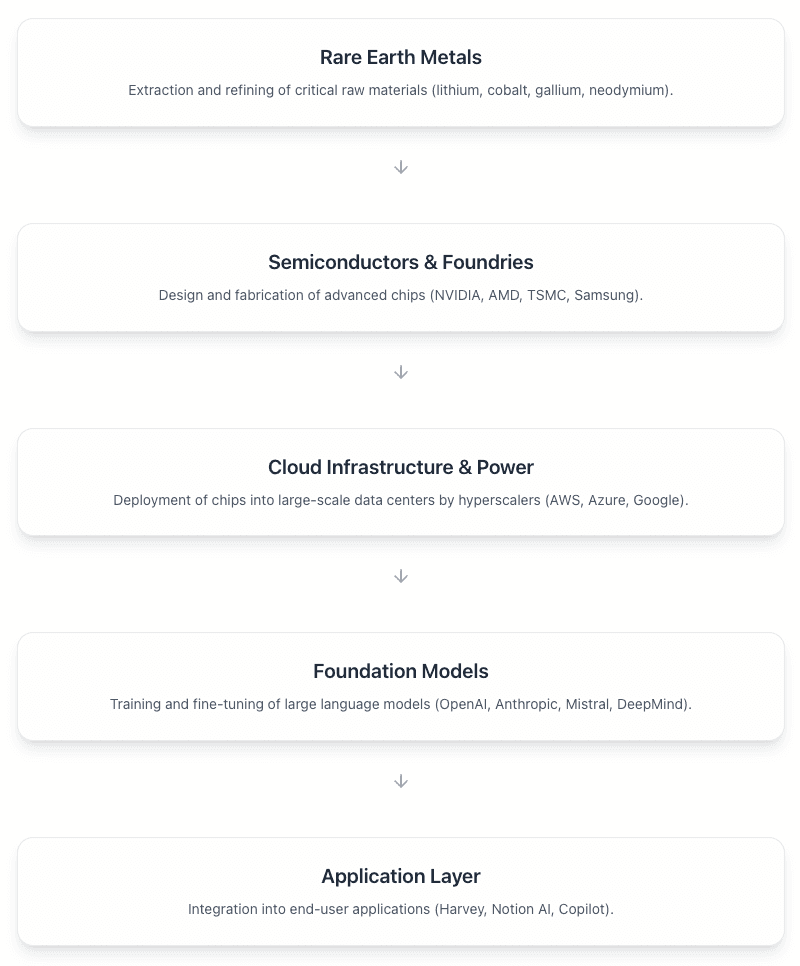

The AI supply chain

To answer the question, we must first break down the sources of variable costs in an LLM-driven application.

We’ll focus on five basic layers: Critical minerals, Chips, Compute Infrastructure, Foundation Models, and finally AI Applications. There are other layers we could add to this. For example, energy is an input into every step. However, this picture captures most of the key players and is rich enough to identify the primary subsidies.

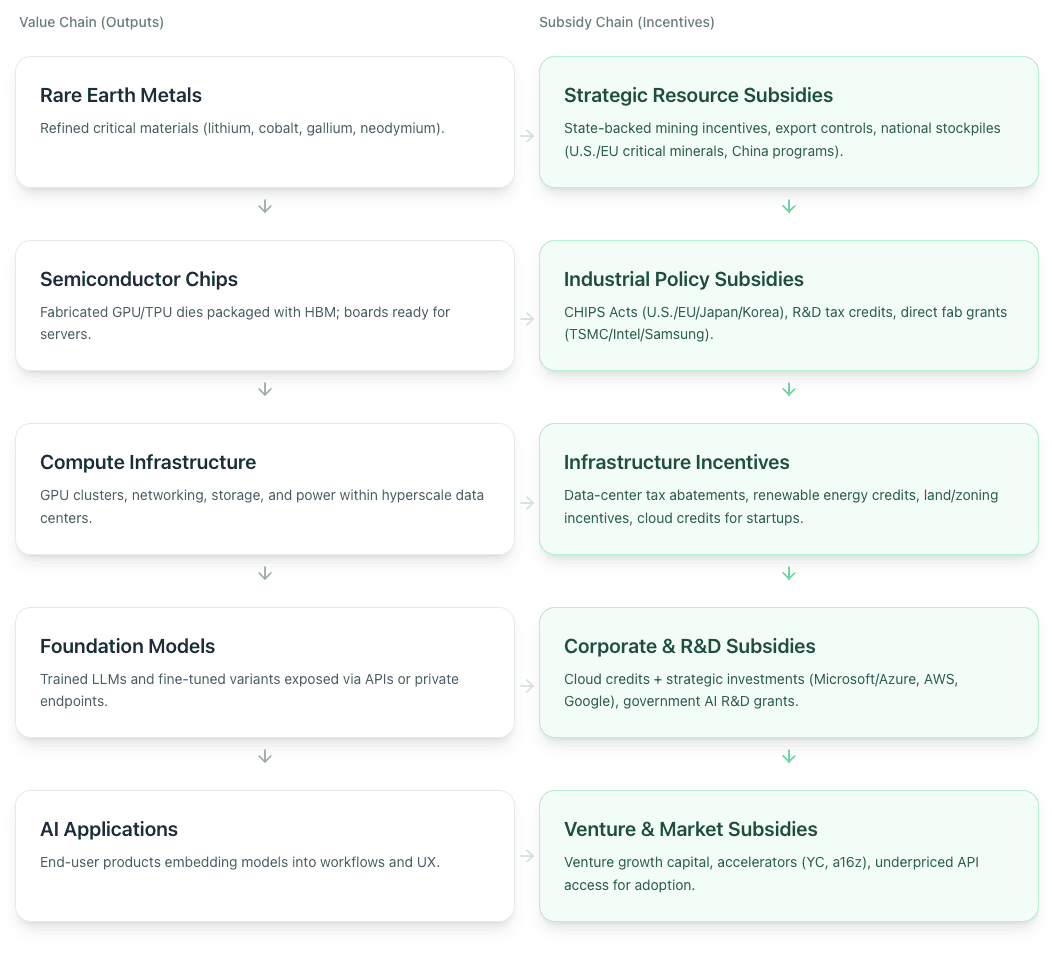

Subsidies in the supply chain

As I reckon is the case with any sufficiently complex and strategic supply chain, there is no shortage of subsidies. However, some of these are more significant than others. To understand the “true cost”, we must identify the most important of these (those that together account for more than 90% of the total subsidization).

As noted above, specific inputs into this supply chain are being ignored. Power is subsidized in many cases but intentionally ignored here—we want to account for a world in which the most temporary subsidies disappear (e.g. those affiliated with the opportunities of a growing market) while leaving the other subsidies that we can expect to remain for years or decades in place (it is unlikely that governments stop subsidizing energy production at the end of an AI wave).

Government subsidies

The most significant government subsidies happen at the most foundational layers. These include discounts on state-backed mining incentives and various programs aimed at reducing the cost of energy.

Fabricators are increasingly viewed as strategic to national interests and receive heavy subsidies, such as those given by the CHIPS Act.

However, few of these subsidies appear to be intimately tied to the AI cycle. Even the U.S. Chips Act is part of a broader arc of government support for the semiconductor industry, despite being ostensibly part of the AI arms race.

As such, we estimate that the effect of short-term government subsidies accounts for <5% of the cost of AI tools in the short term, and so we ignore it in this analysis.

VC subsidies

The most relevant short-term subsidies are those coming from venture capital. Last year alone, 131.5B of venture capital (CB Insights) was poured into AI, accounting for approximately 35% of all venture dollars. That figure nearly doubles when corporate and M&A investment is accounted for (HAI Stanford).

2025 will almost certainly come substantially higher than 2024. Meta alone plans to spend $65 billion on AI investments (Reuters).

But does this decrease the price of models? There is fair anecdotal evidence to suggest a reasonable range for the cost impact at each layer.

For starters, we can fairly confidently ignore the VC subsidies of mining companies and foundries. While there are certainly some cyclical effects as well as many VC-funded start-ups that supply these industries, VC funding in this space is in its infancy (See Pitchbook and SVB).

Similarly, data centers are now a mature industry that has long been weaned off of venture capital. These corporates (Amazon, Microsoft, Google, etc) do provide subsidization to startups—AWS alone has provided hundreds of millions of dollars to startups in free credits (AI Magazine)—but while these might meaningfully change the economics of how startups serve their first couple waves of customers, these subsidies don’t have a meaningful impact once the startup is spending more than a few hundred thousand dollars per year on cloud compute.

As we would expect, it is at the Foundation Model layer and AI Application Layer where VC subsidies have their impact.

The foundation model providers have infamously bad net margins at the moment (Financial Times). Using the most up-to-date public figures for OpenAI, we arrive at an estimate of 60%-70% subsidization by VC.

We can also approach this bottom-up (by examining their cost basis) by using estimates for $/GPU-hr on H100s, rather than the top-down approach (comparing their operating expenses to revenue). We arrived at a similar figure (50% to 65%) using this approach.

At the application layer, the subsidies are generally impacting the contribution margin (accounting for the cost of acquiring customers, i.e., paying for a small army of reps, massive booths, billboards, and marketing material). Nonetheless, without the subsidy, the cost of the service would increase.

The Real Cost of AI Tools

All together, our analysis suggests that the unsubsidized “true cost” of AI tools may be meaningfully higher than the current market cost, just on a cost-basis alone. If AI applications expect to achieve the 70% to 85%+ gross margins that many legacy SaaS tools currently achieve, we would expect the difference between what they “should” charge to be even greater.

The size of this gap varies considerably based on the specifics of the tools. Furthermore, some firms receive steep discounts, meaning the actual cost may be closer to 10 times the license cost. At the same time, other “AI native tools” have relatively low monthly token consumption, decreasing their compute costs, and very possibly putting the “true cost” of the service in line with the current market price.

Will today’s AI tools become more expensive?

If this analysis is correct, then should firms expect the cost of using their current platforms to increase as the market matures?

We don’t think so.

The above analysis assumes constant costs. That is known to be a bad assumption. Software, like most high-technology industries, has deflationary supply-side economics. Holding the size of the models constant, costs fall over time due to both Moore’s Law and algorithmic improvements. In fact, over the past couple of years, we have seen the price per million tokens not just cut in half—which by itself would be a fantastic jump—but in fact it has been cut by 100 times when holding the model constant (HAI AI Index Report). This means that even if VC dollars currently cover 90% of a vendor’s costs, we would still expect a decrease in the cost basis over the next couple of years, even if the VC dollars dry up.

So is your AI platform too cheap? Probably not.

What this means for law firm leaders

Over the past couple of weeks, I’ve heard several innovation leaders express concern over how their AI costs will change over time. This is a natural inclination—associates don’t tend to get cheaper over time.

However, computation has become more affordable every year since the invention of the integrated circuit. I’d bet the farm that this trend will continue beyond the current AI boom.

Legal Bytes

Eve Becomes LegalTech Unicorn — Legal AI startup Eve, which builds tools for plaintiffs’ firms (case evaluation, drafting, discovery), closed a $103M round and achieved a $1B valuation. (Reuters)

Boom in LegalTech Funding Persists — Legal and legal-tech companies have already raised over $2.4B in 2025 (seed through growth), making it the strongest funding year ever for the sector. (Crunchbase News)

Appellate AI Litigation Surges — The number of AI-related appeals is exploding across diverse fields (privacy, trade secrets, §1983, securities), with outcomes at the Supreme Court level likely to reshape the rules of the road. (Bloomberg)

Events

We’ll be speaking on the keynote panel for LegalTech Connect: Innovators & Investors as part of the two-day event happening on October 22-23 in New York at the beautiful space at Ease 605 (located at 605 3rd Avenue). If you’re interested in attending, check out the agenda here. You might be interested if you’d like to rub elbows with:

AI-native LegalTech founders ready to scale

Law firm buyers sharing real adoption signals

Industry insiders mapping the future of legal innovation

VCs and angels looking for investable momentum

Looking to improve your firm's efficiency?

Usually, when we talk about how “cheap “ a tool is, it is in terms of return on investment, rather than the high costs incurred by the provider. It doesn’t matter how cheap a tool is if it isn’t providing ROI.

We’re fortunate to provide our customers with quantifiable metrics and offer some of the highest ROI we’ve seen in the market.

Book a demo to see how PointOne can stop revenue leakage and drive insights across your practice, business, and people.

Thank you for reading, and we look forward to seeing you next week.

Katon